By Sandy Bunch VanderPol

Throughout my entire 43-year career as a self-employed deposition reporter, I’ve prioritized funding my SEP IRA to the maximum amount each year. Not only does this benefit me now that I’m at “retirement age,” but it’s benefited my entire family and will continue to do so into the future. I’ve been paying it forward since I was 24 years old, and my plan is to continue to pay it forward by funding my SEP IRA as long as the law allows me to do such. I would challenge each of you to join me in saving for the future. It is never too late to start.

I’d like to share a few tips I have learned over the course of my career, which have made it possible for me to save for my retirement.

Start your plan today to save for retirement

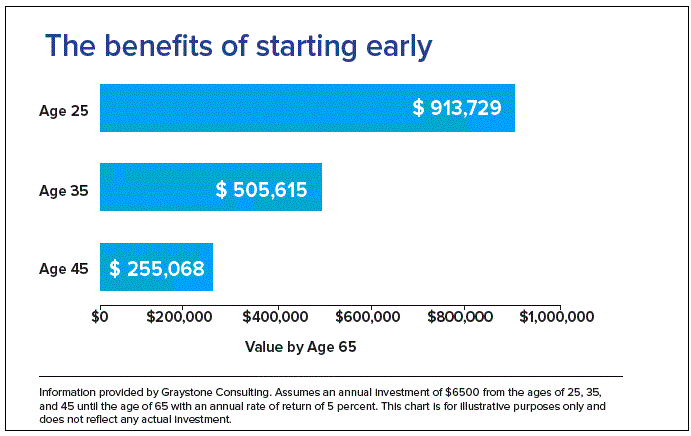

Don’t wait! You can’t rely on social security, the government, or even an inheritance. When I started court reporting at the age of 19, I waited five years to start a SEP IRA. Had I not waited, I would be in an even better financial situation today, thanks to the wonders of compounding interest. It is always tempting to justify waiting another year to start your retirement account, but don’t fall into that trap. Look at the visual below, which is a chart from a wealth management company. I saw a similar one when I was young and it certainly got my attention. I made a plan and started my contributions.

Even if you are starting late, it is important for you to know that you are not alone. Every dollar of investment you put into your retirement account makes a difference. It is never too late.

Each month set aside your retirement contribution

As with my self-employed quarterly tax estimates, I set aside my retirement contribution each month. I’d suggest that you do the same — or, at a minimum, put something into your retirement account each quarter. You don’t have to fund your SEP IRA until April 15th of the subsequent tax year. You can fund your retirement every month or in one lump sum.

Note: Funding your retirement sooner rather than later allows you to earn more on your dollars, depending on how your SEP IRA funds are invested.

I always planned to contribute the maximum amount the law allows to my SEP IRA.

What is a SEP IRA?

A SEP IRA account is an IRA set up for people who own their own small business, and many freelance reporters fall into that grouping. I learned that, as a sole proprietor, I could make annual contributions between 0 to 20 percent of my net adjusted self-employment income (or net adjusted business profits) into my SEP IRA. Also, SEP IRA contributions are very flexible. The percentage of contribution can be changed at any time and may be skipped in a bad year. I didn’t skip any year — I kept up my routine contributions and made my retirement contributions a priority in my budget. SEP IRA contributions are generally 100 percent tax deductible from personal income.

Note: Contributing to your SEP IRA reduces the taxes owed to both the state and the federal government. You can consider this, as I have, as the government helping you to fund your retirement.

Automate your savings

Be disciplined. I set up automatic retirement contributions each month, as this allowed my retirement to grow without having to think about it. Many money management companies have an automated funding service available, and you can often make regular contributions to your SEP IRA from another account within their financial institute and even to self-direct your money to the investments of your choice.

Extra money? Don’t just spend it

My financial advisor used to tell me, “Dedicate at least half of the new money to your retirement plan. And while it may be tempting to take that tax refund or O&5 income and splurge on a new designer purse or a vacation, don’t treat those extra funds as found money. Treat yourself to something small and use the rest to help make big leaps toward your retirement goal.”

So every time I received a check from an O&5 depo, I didn’t spend it – at least not all of it. Instead, I increased my contribution percentage. Remember, the more income you make from your O&5 depositions, the more you can invest into your retirement account, so the more you need to put aside to make the funding.

Make a budget — rein in spending

Sometimes, over the years, my dedication to this goal meant I had to reconsider other things I wanted. I examined my budget and looked at ways to reduce my monthly expenditures, such as insurance costs. As I’ve bought homes, I always looked for one that I was way overqualified for. In other words, I didn’t stretch my budget by buying a higher-priced home. As my income rose, I “moved up” and have finally landed on five acres with a home my husband built and a second modest home in Tahoe. Patience was my friend in this journey.

In conclusion

Good luck on your journey to retirement. There will be many challenges along the way (I want that new car, a bigger house). Keep your retirement goal in mind, front and center. Enjoy the journey of life along the way. Don’t be so frugal you don’t enjoy life. Keep a balance, for sure. Just remember, for every dollar you invest in retirement, it is less you owe in taxes to the government. I was delighted to learn from my CPA this year that, on a side-by-side analysis with the new tax plan, I will be saving between 15-20 percent in taxes due in 2018. So, this money will go to retirement planning or investment planning — as much as I’d love to take a ski trip to Europe.

Sandy Bunch VanderPol, FAPR, RMR, CRR, is a freelance reporter based in Lotus, Calif. She is also credentialed as a Realtime Systems Administrator. She can be reached at realtimecsr@calweb.com.

This article should not be relied on as financial advice specific to your situation. As always, NCRA encourages individuals to reach out to a trusted CPA or other financial advisor to review your personal situation.